Kansas foreclosures soar during year

Despite rise, state ranks well below national average

It’s getting harder for Kansans to hang onto their homes.

The number of home foreclosures in Kansas more than doubled between April 2005 and April 2006, a new report shows.

Still, Kansas remains at roughly half the national rate in terms of the number of home foreclosures, according to the report by the mortgage-tracking service RealtyTrac.

To Kirk McClure, associate professor of urban planning at Kansas University, the numbers mean two things.

First, the low rate compared to the rest of the country means despite Lawrence residents’ often-heard complaints about the rising cost of living here, it isn’t really that bad.

“Kansas in general, and Lawrence in particular, are very affordable housing markets. We are not a costly place to live,” McClure said. “People aren’t stretched. Our incomes aren’t great, but our ratio of house price to income is much more comfortable.”

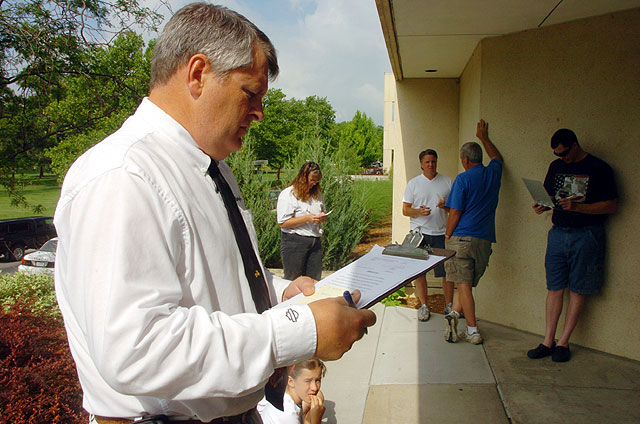

Robin Moore, a Douglas County Sheriff's department employee leads a foreclosed home sale Thursday on the steps of the Douglas County Law Enforcement Center. Moore said he has seen a rise in foreclosures for the weekly sheriff's sales.

Second, McClure said, the jump in the number of foreclosures is a reminder that owning a home isn’t for everyone, even with interest rates as low as they’ve been.

Those “100 percent financed, no-money-down” loans being offered by some lenders as a way to get people into homes can spell trouble for people with irregular incomes, he said.

“I tend to believe that we’ve probably pushed the home ownership rate almost as high as it can be pushed,” he said. “If we take somebody whose income is very low and it’s irregular, and we get them into a home that they can’t sustain two years, three years down the road, we have not done them a service. … There’s a reason why a bank turns somebody down. Maybe what they need to say is, ‘Look, you need to get your savings into a better position.'”

McClure said he thought declining home values in the western part of the state were partly to blame for the foreclosures.

More about local real estate

After all, someone who holds a $100,000 mortgage on a home that drops in value to $90,000 has little incentive to keep paying.

“One of the best tools for our housing markets in western Kansas is a big bulldozer,” he said. “We’ve got too many units.”

Kirk Lowry, vice president of Farmers State Bank in the small town of Atwood in northwest Kansas, said home values there have been holding steady recently as more people move into the area from Colorado.

But he’s seen a handful of foreclosures recently, which he blames on “brain-dead finance companies” that don’t regularly do business in the area.

“They loan well over 100 percent, 125 percent of the value of a piece of property,” he said.

They collect fees that are rolled into the mortgage.

If the owner defaults, he or she has little equity to show for it.

“It’s just as easy to say it’s rent,” he said.

According to the report by RealtyTrac, there were 436 mortgage foreclosures in Kansas in April 2006, slightly more than double the number from April 2005.

The number of foreclosures in Kansas in the first quarter of 2006 was 600, about one-third higher than the 440 foreclosures statewide in the first quarter of 2005.

According to the U.S. Census, the home ownership rate in Kansas in 2005 was 69.5 percent.

According to Census data, that annual percentage rate has changed little since 1984, never rising to more than 72.7 percent and never falling below 66.4 percent.

City Government

City manager’s 2026 proposed budget features flat mill levy but $6.4M in cuts across city’s departments

Lawrence officials, Greek delegation celebrate reaffirmation of 40-year relationship

Lawrence City Commission approves mural that combines Jewish, Kansas imagery for new KU Chabad Center

Lawrence city commissioners approve updated agreements with KDOT for bike, pedestrian projects

On a hot day in Burcham Park, Lawrence’s homeless team hands out popsicles and pet food and builds trust