Financial experts offer planning strategies

Saving early helps you retire in comfort

Bill Wood sure wishes he would have put more money away for retirement.

But at least he has a plan.

“When I retire I would like to find a camp, a youth camp – maybe a church or a 4-H camp – and work, you know. Live there,” Wood says. “They’d pay room and board. I’d either be a maintenance person or, if it’s a livestock or sports kind of thing, I could take care of the animals.”

He’s done the math. As agriculture agent for Kansas State University Research & Extension in Douglas County, Wood figures to collect a federal pension that will pay him at least 50 percent of his federal salary once he retires. The percentage payoff goes up the longer he’s on the job, but the 51-year-old isn’t sure how many more years of work he has left in him.

He just knows he’s not there yet. He can’t be there yet.

“I couldn’t live on that at the moment,” Wood says.

Welcome to the world of retirement planning, where even a dedicated professional with a stable job, a pension and positive work ethic feels like he’s on shaky ground.

Where to turn

Just imagine how many other Lawrence residents feel, with the future of Social Security in question, the stock market battered by a credit crunch and the once-steadfast real estate market – long relied upon in Lawrence as a surefire moneymaker – taking a step back during a nationwide economic downturn.

But that’s no reason to lose hope, financial professionals say.

Don Duncan and Jason Edmonds, vice presidents with Morgan Stanley in Lawrence, continue helping their clients work toward their financial goals. Duncan and Edmonds say they can spend as much as 70 percent of their time working on clients’ retirement plans. The retirement sections of their client reports can stretch as long as 115 pages, looking to factor in as many statistics, expectations and prognostications as possible.

The most important thing, they say, is to plan ahead for living out golden years in relative comfort.

“It’s important to figure out, and it’s not easy,” said Duncan, a certified financial planner.

“It’s not as easy as you would think,” said Edmonds, a portfolio manager. “This is a living, breathing plan. It’s not a one-time, we’ve-got-enough-so-we-don’t-need-to-think-about-it-again kind of thing. It’s a static amount of dollars to turn into a dynamic life of income.”

What to do

While such challenges test even the most seasoned of professionals, financial planners know there are a number of time-tested suggestions for making the best decisions about preparing for retirement:

¢ Start now. Whether you’re fresh out of college, in the middle of a career or fast approaching what are supposed to be your retirement years, fight the urge to put things off. Saving early and often gives you the best chance for making your investments pay off and building a retirement nest egg that can prepare you for whatever comes down the road.

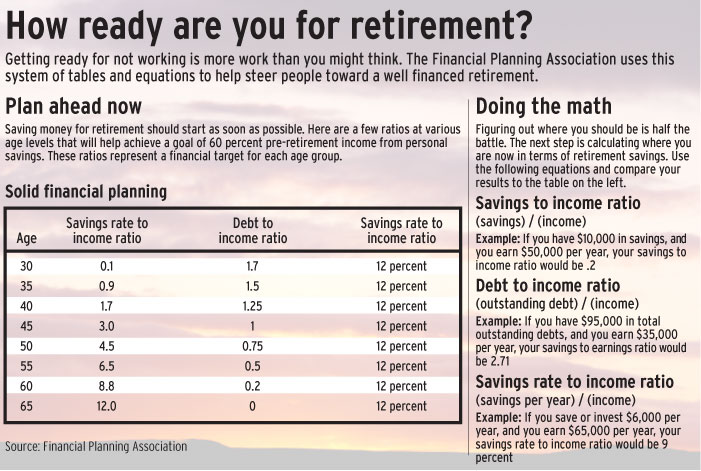

The Financial Planning Association offers the following example: opening a tax-deductible Individual Retirement Account (IRA) at age 25 and investing $100 a month until age 65 would leave you with $349,100 by age 65, assuming an annual return of 8 percent.

Waiting until age 35 to invest the same $100 a month would leave you with $149,035 at age 65, assuming the same 8 percent annual return.

The association’s conclusion: “Waiting 10 years to start saving and investing could cost you over $200,000. : Time will either work for you or against you when saving for retirement, and it’s a lot easier when time is on your side.”

¢ Participate. Take advantage of whatever retirement plan you have available at work.

“Always max out your 401(k),” Edmonds said.

If you can’t afford to do anything else, at least be sure to capture whatever money your employer offers as a “match.” If your employer matches your contributions to the plan up to 5 percent of your salary, then contribute at least 5 percent of your salary to your plan.

“It’s like ‘free money,'” according to the FPA. “Where else can you get this kind of return on your investment?”

The association suggests putting at least 10 percent of your pre-tax income into the plan. The money is deducted from your paycheck on a pre-tax basis. If that’s too much to save, go for a smaller amount and find other ways to save – by contributing half of your next raise, for example.

¢ Adjust. As you age into your 50s and 60s, try to put 20 percent or more of your income into your retirement savings, the FPA recommends. While a portion of your investments likely should be shifted into less-volatile assets, such as bonds, many planners still recommend maintaining a “substantial exposure” to stocks.

“You still have a lot of years ahead of you, both to reach retirement and during retirement itself,” the association says. “You’ll need some assets that can help you stay ahead of inflation and preserve (the) purchasing power of your income.”

Looking to the future

Wood, who spends his work days advising farmers and ranchers how to get the most out of their own agricultural resources, knows the advice. For a time, he even worked a bit in insurance and investments.

“You need to save when you’re young and on a regular basis to have a good retirement,” Wood says.

That’s why he and his wife, Robin, are “pumping any spare cash we have” into an IRA, to help make up for the conscious decisions they’d made to forego some – not all – of their retirement savings as their children were growing up.

But he also understands how too many others are living beyond their means, postponing all savings and relying on credit cards to get them through until – what? – it’s time to retire?

“If all they have is Social Security, they’ll be in poverty,” Wood says.

Wood is thankful that he’s not facing such a future. The federal pension forms the base. Social Security will add more. The IRA will build value.

Then it’s a matter of managing expenses and, yes, getting a job.

“I can’t imagine just watching TV or playing golf all day,” Wood says. “Some people can do that, and that’s OK. But I like doing things, and I’ll be doing something to fill up my time.”