Low rates draw young buyers

Chicago ? Record-low interest rates are prompting people in their early 20s to do something they hadn’t thought possible at their age: buy a home.

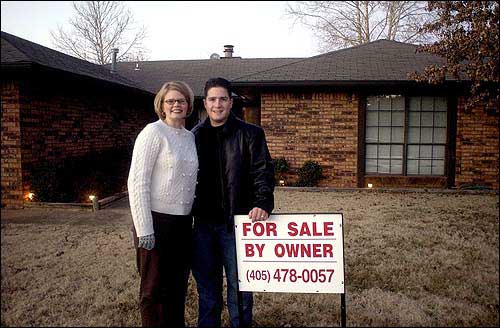

Erin Engelke was a fresh-faced college graduate when she and her husband Jason bought their first home, a townhouse in Edmond, Okla. They’ve since bought another three-bedroom house and rent the townhouse to college students. She’s 24. He’s 25.

Cristi Cola recently moved into a little two-bedroom house in Safety Harbor, Fla. — “just perfect for a single girl like me,” the 23-year-old says.

Jeff Lischett, also 23, used his signing bonus and a salary advance from Kraft Foods to fill out the down payment he’d started saving while living with his dad after college graduation. He’ll be moving into his new two-bedroom, two-bath townhouse in suburban Chicago later this month.

“Most people my age realize that renting is silly when you think about it,” says Lischett who got a 5 percent interest rate that makes his monthly mortgage payments comparable to — or even less than — he would have paid in rent.

“And living at home for a couple years to save money isn’t as frowned upon anymore,” he says. “You’re no longer the loser living in the basement.”

While Lischett was able to come up with his own 10 percent down payment, many buyers his age are getting help from parents or grandparents. Still others are taking advantage of deals — prompted by a hot buying market — for 5 percent down payments or even those that require no money down.

The current climate is making it possible for some young people to buy “even in New York City,” says Ellen Bitton, CEO of Park Avenue Mortgage Group Inc., a lender that does business in many states. She says most homebuyers 25 and younger are seeking loans in the ballpark of $130,000 to $350,000.

Real estate industry statistics show the impact.

The median age of the first-time homebuyer has been dropping — from age 32 in 1999 to 31 in 2001, according to a survey done every other year by the National Association of Realtors. And transactions from the under-25 crowd rose from 305,192 in 1999 to 321,136 two years later. Overall, there were 2.85 million first-time buyer transactions in 1999 and 3.09 million in 2001.

Though it’s creating headaches for apartment landlords in some cities — who rely on twentysomethings for rent — experts say financially stable young people who buy property have an unprecedented opportunity — to get loans at record-low rates and to begin building equity in a home earlier than some of their parents did.

Erin and Jason Engelke stand in front of the home they recently purchased in Edmond, Okla. Record-low interest rates are prompting people in their early 20s to do something they hadn't thought possible at their age: buy a home.

“Homes for these young families are not just a place for them to lay their heads at night. These are little prosperity factories,” says Scott Syphax, president and CEO of the Nehemiah Corporation of California, a nonprofit organization that provides homebuyers with down payment assistance.

The trend is causing some real estate agents to target young buyers. A few agents at the RE/MAX real estate firm, for example, host first-time buyer seminars for college students.

Other agents say savvy twentysomethings are coming to them.

“They’re not going for the flash. They’re not going for the fancy cars. They’re going for the real estate,” says Honore Frumentino, a broker with Koenig & Strey GMAC Real Estate in Deerfield, Ill.

Of course, real estate is not a surefire investment. And for those who graduate from college saddled with hefty student loans and credit card bills, getting deeper in debt may not be the right move.

“We don’t want to strap young people with so much debt and responsibility that they get themselves into a bad cycle,” says Dovie Morgan, vice president of Heritage Texas Properties in Houston.

Some young buyers also admit that making monthly mortgage payments is not always easy.

Meredith Fretz, a 25-year-old who recently bought an 100-year-old stone townhouse in Manayunk, Pa., says she has to have a roommate to help her afford the mortgage.

Teha Kennard also says money’s been tight — but in a good way.

“Now that I am in debt, I am very aware of my finances,” says the 24-year-old, who bought a condo in Washington in October. “I am also more focused on saving.”

In the end, many say taking on the responsibility of a home is worth it.

Says 24-year-old homeowner Kevin Jurrens of Hamilton, N.J.: “When I sit in my recliner, I can look around and be proud of the fact that at this age, I own my very own house.”